Have you ever stared at a prescription bill, wondering why your insurance copay jumped from $5 to $50 overnight? Or perhaps you switched to an online pharmacy for convenience, only to find out your insurance wouldn't cover the transaction at all. You are not alone. The intersection of insurance coverage is financial protection that pays for part or all of medical costs, including prescriptions, online pharmacies are internet-based retailers that dispense medications directly to patients' homes, and generic drugs are medications with identical active ingredients to brand-name versions but lower prices is messy. It’s filled with jargon, hidden rules, and distinct channels that look similar but work very differently.

If you want to save money on your meds without getting hit with surprise bills, you need to understand how these pieces fit together. This isn’t just about picking the cheapest pill; it’s about knowing which digital doors your insurance will actually let you walk through.

The Difference Between Mail-Order and Independent Online Pharmacies

This is the biggest trap people fall into. When we say "online pharmacy," we usually mean two completely different things. Getting them mixed up can cost you hundreds of dollars.

First, there is the mail-order pharmacy is a service integrated into health insurance plans that delivers maintenance medications directly to your home. These are not independent websites. They are part of your insurance plan’s network, often managed by a pharmacy benefit manager (PBM) is an intermediary organization that manages prescription drug benefits for health insurers like Express Scripts, CVS Caremark, or Optum Rx. If your plan includes mail-order, using it is seamless. Your insurance card works instantly, and you pay the exact copay listed in your plan documents-often significantly lower than retail.

Second, there are independent online pharmacies. Think of Amazon Pharmacy, Walgreens.com, or smaller specialty sites. These operate more like e-commerce stores. While some accept insurance, many do not. If you order from an independent site that isn’t in your PBM’s network, your insurance might reject the claim entirely. You’d have to pay the full cash price upfront and then file for reimbursement later-which rarely results in a full refund. Always check if the specific website is an authorized provider for your plan before entering your credit card details.

How Generic Drug Tiers Dictate Your Cost

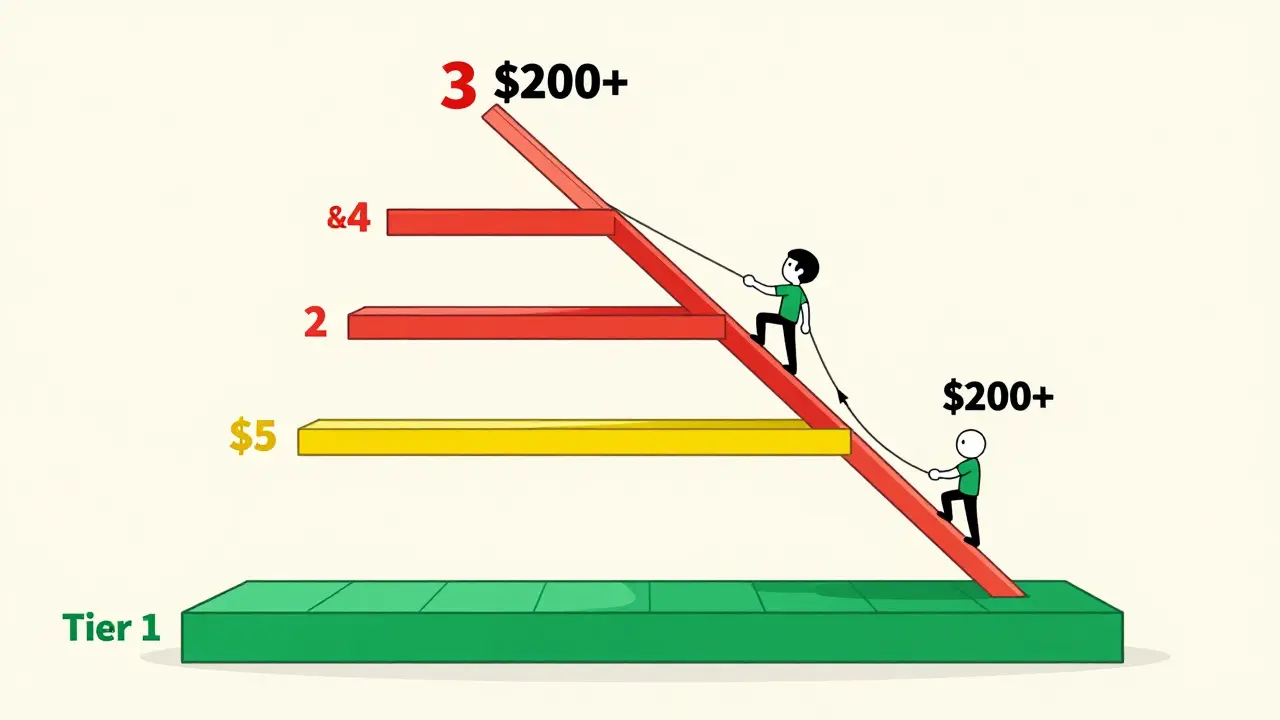

Your insurance plan has a list of covered drugs called a formulary is a list of prescription drugs covered by a health insurance plan. This list is divided into tiers. Where your generic drug sits on this ladder determines what you pay.

- Tier 1 (Preferred Generics): These are the cheapest options. Most plans charge a flat fee, such as $5 for a 30-day supply or $10 for a 90-day mail-order supply. This is where most standard generics live.

- Tier 2 (Non-Preferred Generics): Some generics are less preferred by the insurer, perhaps because they aren’t as widely used or have specific contract issues. Here, you might face higher coinsurance, meaning you pay a percentage of the cost rather than a flat fee.

- Tier 3 & 4 (Brand Name): If you refuse the generic and demand the brand name, you jump to these tiers. Costs skyrocket, often involving high deductibles or coinsurance capped at $200 or more per prescription.

For example, data from federal health plans shows a clear incentive structure: a 30-day generic supply at a retail pharmacy might cost $5, while a 90-day supply via mail-order costs $10. That’s a 33% savings per dose. But this only works if your medication is on Tier 1. If your doctor prescribes a non-preferred generic, those low copays vanish. Always verify your drug’s tier status using tools like Aetna’s medicine search or your insurer’s app before switching pharmacies.

The Reality of "Non-Medical Switching"

You’ve probably heard your pharmacist ask, "Do you want the generic?" But sometimes, the switch happens without asking. This is known as non-medical switching is the practice of insurers requiring patients to take generic drugs instead of brand names regardless of physician preference.

Insurers are under pressure to cut costs. According to healthcare attorney Scott Glovsky, this trend is driven by cost containment, not necessarily medical necessity. In 2023, major PBMs expanded their "generic-only" tiers to include 127 additional medication classes. If your doctor writes for a brand-name drug that has a generic equivalent, your insurance may automatically substitute the generic-or deny coverage for the brand unless your doctor fights for it.

This creates a friction point. Some patients report severe side effects when switched unexpectedly. For instance, a multiple sclerosis patient reported being switched from Copaxone to a generic without consultation, leading to emergency room visits. If you feel a generic isn’t working, don’t just suffer in silence. Ask your doctor to request a formulary exception is a formal process allowing a patient to receive a non-covered drug due to medical necessity. This requires prior authorization, which can be a hassle, but it’s the legal pathway to get back on the medication that works for you.

When Cash Price Beats Insurance Copay

Here is a counterintuitive truth: sometimes, paying cash for a generic at an online or retail pharmacy is cheaper than using your insurance. This happens frequently with high-deductible health plans.

Consider Walmart’s generic program, which offers dozens of common generics for $10 for a 90-day supply. If your insurance plan has a $2,000 deductible and hasn’t been met yet, your copay might be 100% of the drug’s cost. If the drug costs $15, paying $10 cash saves you $5. More importantly, paying cash doesn’t count toward your deductible in the same way, though it also doesn’t help you reach the out-of-pocket maximum faster. It’s a trade-off.

New models like Amazon Pharmacy’s RxPass is a subscription service offering unlimited refills of select generic medications for a flat monthly fee complicate this further. For Prime members, it costs $5/month for up to 15 eligible generic prescriptions. If you take three generic meds, that’s $1.66 per drug per month-beating almost any insurance copay. However, RxPass is limited to specific drugs and doesn’t cover specialty medications. It’s a powerful tool for simple, chronic conditions but useless for complex regimens.

| Channel Type | Typical Cost Structure | Insurance Integration | Best For |

|---|---|---|---|

| Mail-Order (Plan Network) | $5-$10 for 90 days | Seamless; uses insurance ID | Maintenance meds (blood pressure, cholesterol) |

| Independent Online Pharmacy | Varies; often cash price | Inconsistent; check acceptance first | Convenience; if cash price < copay |

| Retail Pharmacy (In-Network) | $5-$15 for 30 days | Seamless; instant verification | Immediate needs (antibiotics, acute care) |

| Subscription Models (e.g., RxPass) | $5/month flat fee | None; separate payment | Multiple stable generic prescriptions |

Navigating Prior Authorization and Delivery Delays

Switching to an online channel isn’t always plug-and-play. Mail-order pharmacies typically require a 90-day supply. This means your doctor must write a script for three months’ worth of pills. While this sounds efficient, it introduces delays. GoodRx notes that mail-order delivery takes about one week. If you run out of meds before the new shipment arrives, you’re stuck.

Furthermore, 18% of mail-order requests require prior authorization, according to MHBP data. This means the PBM reviews your case to ensure the drug is medically necessary before approving coverage. This process can add days or weeks to your wait time. For acute issues like infections or post-surgery pain, mail-order is a poor choice. Stick to local retail pharmacies for immediate needs.

To avoid gaps in treatment, plan ahead. Request your 90-day refill two weeks before you expect to run out. Use your insurer’s mobile app to track shipment status. And remember, if you travel, mail-order might not be feasible. Keep a small backup supply at home for emergencies.

Practical Steps to Verify Coverage

Don’t guess. Verification is free and takes minutes. Here is how to protect yourself:

- Check the Formulary: Log into your insurer’s portal or use tools like CVS Caremark’s "Check Drug Cost & Coverage." Enter the first three letters of your medication name. See which tier it falls into.

- Confirm Mail-Order Eligibility: Call the number on the back of your insurance card. Ask specifically: "Does my plan include mail-order pharmacy benefits for generic drugs?" Note any restrictions on drug types.

- Compare Cash Prices: Use apps like GoodRx or Cost Plus Drugs to see the cash price of your generic. Compare this to your insurance copay. If the cash price is lower, consider paying out-of-pocket.

- Verify Independent Pharmacy Acceptance: If you prefer a specific online retailer, call their customer service. Ask: "Do you accept [Your Insurance Plan] directly?" Do not assume they do.

- Understand Reimbursement Policies:** If you must use an out-of-network online pharmacy, ask your insurer about the reimbursement process. Will they reimburse based on the allowed amount or the actual paid amount? The difference can be significant.

Knowledge is power here. The system is designed to favor the insurer’s preferred vendors and lowest-cost drugs. By understanding the mechanics of formularies, PBMs, and network structures, you can navigate around the pitfalls and keep your healthcare costs predictable.

Does insurance cover generic drugs from any online pharmacy?

No. Insurance typically only covers drugs from pharmacies within its network. This includes plan-specific mail-order services and certain partnered online retailers. Independent online pharmacies may not accept your insurance, requiring you to pay cash and seek partial reimbursement later, which is often incomplete.

What is the difference between mail-order and regular online pharmacy?

Mail-order pharmacies are integrated into your insurance plan’s PBM network, offering seamless billing and lower copays for 90-day supplies. Regular online pharmacies are independent entities that may or may not accept your insurance, functioning more like standard e-commerce stores.

Why would my insurance force me to take a generic?

This is called non-medical switching. Insurers use formulary exclusions and high brand-name copays to encourage generic use, saving millions in costs. Generics have identical active ingredients and are clinically equivalent for most patients, making them a cost-effective alternative.

Is it cheaper to pay cash for generics than use insurance?

Sometimes. If you have a high-deductible plan, your insurance copay might be the full retail price. Programs like Walmart’s $10 generic list or Amazon RxPass ($5/month) can be significantly cheaper than insurance copays for certain medications. Always compare prices before filling.

How long does mail-order pharmacy delivery take?

Typically about one week. Because of this delay, mail-order is best for maintenance medications like blood pressure or cholesterol drugs. It is not suitable for acute needs like antibiotics or post-surgery pain management, where immediate access is required.

Naresh Chandra

I feel your pain deeply!! The system is so broken!!! I spent hours on the phone with my insurer last week!!! They kept transferring me to different departments!!! It was exhausting!!! But this guide is a lifesaver!!! Thank you for breaking it down!!!

Joseph Teichman

good read. i use goodrx all the time now. saves me cash every month. insurance copays are a joke.

Grace Gayle McMullen

honestly this is why i switched to amazon rxpass. its just easier than dealing with the mail order headaches. my blood pressure meds are covered and i dont have to worry about tiers anymore. though i did misspell formulary in my notes lol.

Gareth Tyler

interesting points. but does anyone else think the delivery times are too long? waiting a week for meds feels risky if you get sick suddenly. maybe keep some at home?

Jonhnnie john13

the article ignores the fact that PBMs are price fixing cartels. they manipulate formularies to force generics not because of efficacy but because of rebates. consumers are pawns in their profit game.

Cyburg Adeoye

You are absolutely right about the PBM dynamics! It is crucial to understand the underlying pharmaceutical economics! We must empower ourselves with knowledge! Let us support each other in navigating these complex healthcare landscapes! Together we can find better solutions!

Sharon O’Mahonh

i mean yeah its messy but sometimes you just gotta pay cash. its simpler than fighting the bureaucracy. life is short why waste energy on insurance claims when you can just buy the drug and move on with your day?

Angela Niculescu

actually i disagree with the mail order push. retail pharmacies are faster and more reliable. plus you can talk to a pharmacist face to face. online feels impersonal and risky.

Victoria Mangiapane

boring article. everything here is common sense. who reads this stuff anyway? just pay the bill and stop complaining. typical whining from people who should have read the fine print.

Russell Russell

We need to shift our mindset towards proactive health management. Knowledge is indeed power. By understanding the nuances of insurance coverage, we take control of our well-being. Let us inspire others to do the same. Empowerment starts with information.