When your insurance plan drops your medication from coverage or moves it to a higher cost tier, it’s not just a paperwork issue-it’s a threat to your health. Thousands of people face this every year, often with little warning. A drug that’s been working for years suddenly becomes unaffordable, and you’re left scrambling. This isn’t rare. In 2024, 34% of Medicare beneficiaries experienced a formulary change that affected their medication, and 47% of patients abandoned their prescription when it moved from tier 2 to tier 3. If you’re on a chronic medication like insulin, Humira, or blood pressure pills, you need to know how to handle these changes before they hit you hard.

What Is a Formulary, Really?

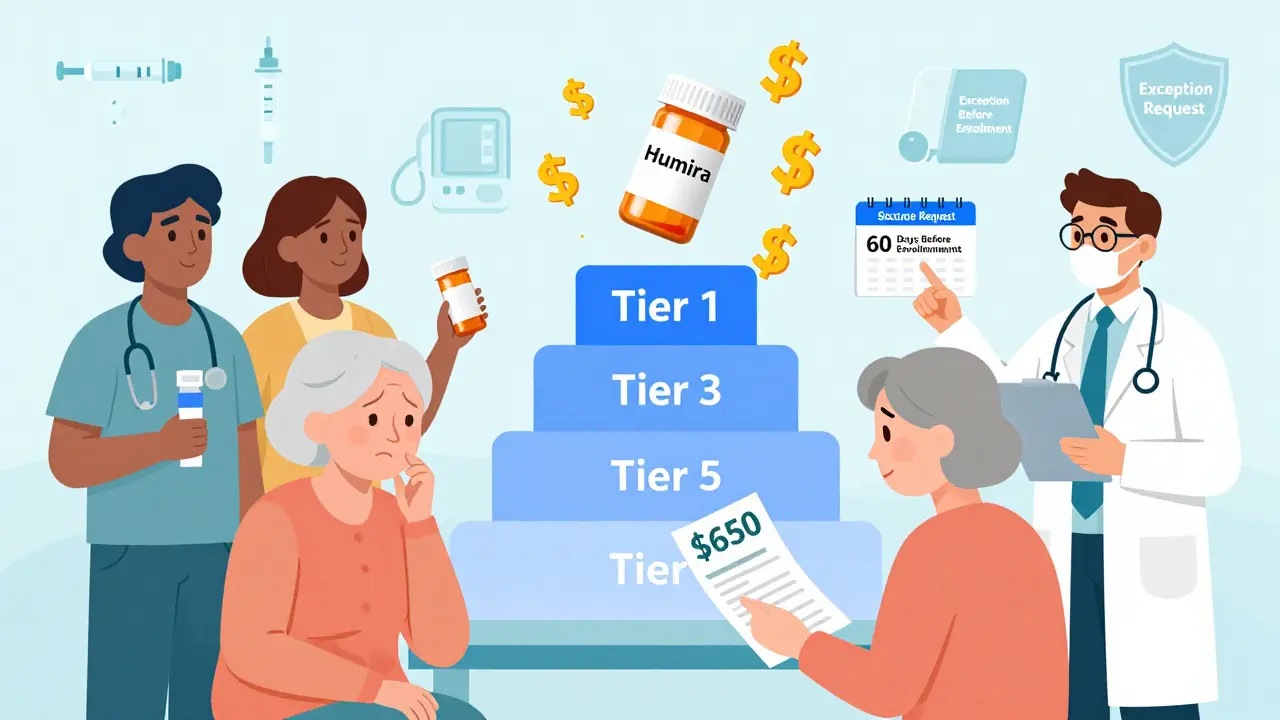

A formulary is simply a list of drugs your insurance plan covers. But it’s not just a list-it’s a ranking system. Most plans use a tier structure: tier 1 (cheapest generics), tier 2 (preferred brands), tier 3 (non-preferred brands), and tier 4 or 5 (specialty drugs). The higher the tier, the more you pay out of pocket. For example, a diabetes drug on tier 2 might cost you $30 a month. Move it to tier 3, and that jumps to $150. Move it to tier 5? You could be paying $600 or more.

Medicare Part D plans are required by law to cover at least two drugs per therapeutic class, but that doesn’t mean they’ll cover the one you’re on. Commercial insurers have even more flexibility. In fact, 92% of Medicare Part D plans and 87% of commercial plans use tiered formularies. The goal? Control costs. But the trade-off is often patient access.

Why Do Formularies Change?

Changes happen for three main reasons: cost, competition, and clinical evidence.

- Cost: If a new generic enters the market, insurers will push it to tier 1 and bump the brand-name drug up. If a drug’s price spikes, the plan may drop it entirely.

- Competition: Insurers negotiate rebates with drug makers. If a company offers a bigger discount, the plan may swap out a competing drug-even if it’s working fine for you.

- Clinical evidence: Sometimes, new studies show a drug is less effective or riskier than alternatives. The plan’s Pharmacy and Therapeutics (P&T) committee reviews this data quarterly and may remove it.

Most large insurers review formularies every three to six months. You might not hear about it until you go to fill your prescription and get a surprise bill. That’s why proactive monitoring matters.

How Formulary Changes Hit Real People

Take the story of a patient on Humira for Crohn’s disease. For seven years, their plan covered it at a $50 copay. Then, without warning, it moved to the specialty tier. Their monthly cost jumped to $650. They had no idea this was coming. They didn’t get a letter until after the change took effect. They spent three weeks fighting for a temporary exception while their symptoms flared. That’s not an outlier-it’s standard.

GoodRx data shows that when drugs move from tier 2 to tier 3, abandonment rates jump by 47%. For diabetes medications? It’s 58%. Why? Because many patients can’t afford the jump. And when they stop taking their meds, they end up in the ER, on dialysis, or hospitalized-costing the system far more in the long run.

On the flip side, clinics with proactive systems are seeing better outcomes. One practice in Arizona started checking formulary status 60 days before open enrollment. They switched 80% of at-risk patients to alternatives during routine visits. No disruptions. No crises. Just smart planning.

What You Can Do Before a Change Hits

You don’t have to wait for a surprise. Here’s how to stay ahead:

- Check your formulary every year. During open enrollment (October to December for Medicare, anytime for commercial plans), log into your insurer’s website and search for your exact drug name. Don’t rely on last year’s list.

- Use official tools. Medicare beneficiaries can use the Plan Finder tool (used by 68% of users in 2023). Commercial plan members should use their insurer’s formulary lookup-available on 92% of health plan websites.

- Ask your pharmacist. Pharmacists see formulary changes daily. Ask them: "Is my med still covered?" during your next refill.

- Set calendar reminders. Mark 60 days before your plan year ends. That’s when most changes are announced.

If you’re on a specialty drug, keep a printed copy of your current coverage. You’ll need it if you have to appeal.

What to Do When Your Drug Is Removed

If your medication is taken off the formulary or moved to a higher tier, you have options. Don’t panic. Don’t stop taking it. Act.

- Request a formulary exception. You can ask your insurer to cover your drug anyway. You’ll need a letter from your doctor explaining why the alternative won’t work. 64% of medically justified exceptions are approved. For urgent cases (like cancer or organ transplant drugs), CMS requires plans to respond within 72 hours.

- Try a therapeutic alternative. Your doctor might have a similar drug on a lower tier. For example, if your blood pressure med is dropped, there are often 5-8 other options in the same class. Don’t assume they’re all the same-some have fewer side effects or better long-term outcomes.

- Use manufacturer assistance. Drug companies offer copay cards or free programs for eligible patients. In 2024, these programs covered $6.2 billion in patient costs. Check the manufacturer’s website or ask your pharmacist.

- Appeal if denied. If your exception is denied, you have the right to appeal. Medicare beneficiaries can call their State Health Insurance Assistance Program (SHIP). Users who used SHIP had a 37% higher success rate.

How Providers Can Help

Doctors and pharmacists are on the front lines. Many now use e-prescribing systems that check formulary status in real time. That means before a script even leaves the office, the system flags if the drug is covered-or if a cheaper alternative exists.

Large medical groups with these systems report 76% of prescriptions are verified before being sent. That cuts down on delays, refusals, and patient frustration. If your provider doesn’t do this, ask them to. You’re not just a patient-you’re a partner in your care.

What’s Changing in 2025 and Beyond

The rules are shifting fast. Starting in 2025, the Inflation Reduction Act caps Medicare out-of-pocket drug costs at $2,000 per year. That’s huge. It means insurers can’t push patients into high tiers without consequences. We’ll likely see fewer extreme tier jumps and more focus on value-based formularies-where drugs are chosen based on real-world outcomes, not just price.

Also, by 2025, Medicare Part D must standardize how exceptions are handled. Right now, each plan has different rules. That’s confusing. Standardization will make appeals easier.

Long-term, experts predict personalized formularies. Imagine a system that looks at your genetics, past response to meds, and even your lifestyle to build a drug list just for you. It’s not sci-fi-it’s coming. 68% of industry leaders expect this within the next decade.

Key Takeaways

- Formulary changes are common, predictable, and often sudden.

- Always check your drug’s coverage before open enrollment.

- Don’t wait for a bill to act-monitor your plan proactively.

- You have rights: exceptions, appeals, and manufacturer help are real tools.

- Work with your provider and pharmacist. They’re your best allies.

Managing formulary changes isn’t about fighting your insurer. It’s about staying informed, prepared, and persistent. The system isn’t perfect-but you’re not powerless.

How often do insurance plans change their formularies?

Most commercial insurers review formularies every three to six months, with major changes announced during open enrollment. Medicare Part D plans must give 60 days’ notice for non-urgent changes and are required to review new drugs within 120 days of FDA approval. Some plans make small tweaks monthly, while major shifts happen once or twice a year.

Can I be switched to a different drug without my doctor’s approval?

No. Your insurer can’t force you to switch unless they give you a valid alternative and allow you to request an exception. Even then, your doctor must agree to the change. If you’re switched without consent, file a complaint with your state insurance commissioner or Medicare. Many patients report being switched without notice-this is a violation of transparency rules.

What’s the difference between a tier 3 and tier 4 drug?

Tier 3 drugs are typically non-preferred brand-name medications with higher copays-often $100-$150 per month. Tier 4 (or specialty tier) drugs are high-cost, complex treatments like biologics, cancer drugs, or rare disease therapies. These often require prior authorization and can cost $300-$1,000+ monthly. Coinsurance (a percentage of the cost) is common in tier 4, not a flat fee.

Do all insurance plans use the same formulary tiers?

No. Medicare Part D plans must follow federal rules and typically have six tiers. Commercial plans vary: some have three tiers, others have five or six. Some use value-based tiers that reward drugs with proven outcomes, not just low cost. Always check your specific plan’s formulary document-it’s usually available online under "Drug Coverage" or "Formulary."

Can I switch plans mid-year because of a formulary change?

Generally, no. You can only switch Medicare plans during open enrollment (Oct 15-Dec 7) or if you qualify for a Special Enrollment Period (like moving or losing other coverage). For commercial plans, some employers allow mid-year changes if your drug is removed. Always ask your HR department or insurer-they may have flexibility you didn’t know about.

What if my drug is completely removed from the formulary?

You’re still entitled to a transition supply. Medicare and many commercial plans must give you at least a 30-day supply of your discontinued drug-even if it’s no longer covered. Some offer up to 60 days. Use this time to work with your doctor on alternatives or file an exception. Never stop taking your medication cold turkey.

Milad Jawabra

This is the kind of info that saves lives. I’ve seen friends stop their insulin because of a tier shift - one ended up in the ER. Don’t wait for a bill. Check your formulary like it’s your Netflix subscription. Set a damn calendar alert. Your body doesn’t care about corporate budget cycles. 🚨

Jessica Chaloux

I just got hit with this last month. My Humira went from $45 to $720. I cried in the pharmacy. My doctor didn’t even know until I told him. 😭 Why do they do this to people who are already sick? It’s not healthcare - it’s a gamble with your life.

Mariah Carle

The real tragedy isn’t the tier system - it’s the illusion of choice. We’re told we have "options," but the only real option is to beg for mercy from a bureaucracy that profits from your suffering. Capitalism doesn’t heal. It just rebrands pain as a cost center. 🤔

Megan Nayak

You people are missing the forest for the trees. The problem isn’t formularies - it’s that we let pharmaceutical companies set the agenda. They lobby, they bribe, they buy off P&T committees. And we act surprised when our insulin costs more than our rent? Wake up. This is systemic. Not a glitch - a feature.

Divya Mallick

In India, we don’t have this luxury. We pay cash. We negotiate. We split pills. We don’t wait for a letter. If your insurance drops your drug, go to a local chemist, ask for the generic, and buy it for 10% of the price. Stop acting like you’re entitled to corporate healthcare. You’re not a customer - you’re a patient. Act like one.

Pankaj Gupta

Divya makes a valid point. In many developing nations, access is determined by affordability, not formulary tiers. The U.S. system is not broken - it was designed this way. Profit-driven care is not an accident. It’s the architecture. The solution isn’t better alerts - it’s systemic overhaul.

Alex Brad

Check your formulary. Every year. 60 days before renewal. Do it now. Seriously. It takes 3 minutes.

Renee Jackson

Thank you for this meticulously detailed and compassionate guide. Proactive health management is not merely advisable - it is an ethical imperative. I have shared this with my entire care team, and we are implementing a quarterly formulary audit protocol across our clinic. Your clarity is a beacon in a fog of administrative chaos.

Richard Elric5111

The deeper philosophical question here is not whether we can navigate formularies, but whether a healthcare system predicated on market logic can ever be just. If a diabetic’s life is contingent on a corporate rebate negotiation, then we have abandoned medicine as a human right and reduced it to a commodity. The tier system is not a policy - it is a moral failure.

Dean Jones

Look, I’ve been on the same med for 12 years. My plan changed it twice. First, they moved it from tier 2 to tier 3 - fine, I paid. Then they dropped it entirely. I filed an exception. Got denied. Filed an appeal. Took 47 days. My doctor wrote a 12-page letter. They approved it on the 48th day. Meanwhile, I was taking half doses because I couldn’t afford the full one. I’m alive. But I’m not okay. And I’m not alone. The system is rigged. It’s not about knowing how to fight - it’s about having the time, energy, and privilege to fight at all. Most people don’t. And that’s the real crisis.

Betsy Silverman

I work in a community clinic. We’ve started using real-time formulary checkers during intake. It’s changed everything. No more "I didn’t know" or "I can’t afford it". We catch issues before they become emergencies. It’s not glamorous. But it’s life-saving. If your provider doesn’t do this - ask them to. You’re not being difficult. You’re being smart.

Ivan Viktor

So you’re telling me the solution to a $600 insulin bill is to... check a website? Cool. Meanwhile, my cousin’s kid is on a ventilator because they couldn’t afford their nebulizer. I’ll take my sarcasm and my lack of emoticons and go cry in a parking lot now.